Your grounds care provider is scheduled for a routine visit. The crew shows up, starts edging, and an irrigation valve fails behind the building. Water runs for hours before anyone notices. By the time your tenant calls, you're dealing with damaged turf, a soaked walkway, and a fresh argument over who pays.

That's the essential job of commercial landscaping insurance. It's not paperwork. It's a financial firewall between your property budget and someone else's mistake.

If you manage office, retail, industrial, hospitality, healthcare, or HOA properties, you need to treat landscaping insurance as part of vendor risk control. Not admin. Not purchasing. Risk control. The landscaping industry is too large and too active for casual oversight. IBISWorld projects U.S. landscaping services industry revenue at $176.7 billion in 2026 across 556,000 businesses, and the broader market includes more than 1.4 million employees and 692,777 landscaping service businesses reported by NALP through that same industry reference. That scale means one thing for property managers: you're hiring from a massive contractor pool, and you can't assume every vendor manages risk the same way.

Table of Contents

- Why Your Landscaper's Insurance Matters

- The Core Four Insurance Policies for Landscapers

- Advanced Coverage for Specialized Landscaping Risks

- How to Read a Certificate of Insurance

- Essential Contract Clauses for Risk Transfer

- Real-World Scenarios and Best Practices

- Frequently Asked Questions about Landscaping Insurance

Why Your Landscaper's Insurance Matters

Most landscaping losses start small. A broken window. A worker injury. A truck backs into a gate arm. Then the invoices arrive, attorneys get copied, and the “routine vendor” suddenly becomes a liability problem for ownership.

That's why you need to think in one phrase: risk transfer. If your contractor causes damage or one of their employees gets hurt, their insurance should respond first. If you skip verification, your property may end up absorbing costs that should never have touched your operating budget.

Insurance is how you move risk off your books

A commercial landscaping contract isn't just a service agreement. It's a transfer document. You're hiring someone to perform physical work on your site with vehicles, crews, sharp tools, powered equipment, and often irrigation systems tied to water flow and hardscape.

When that work goes wrong, the insurance structure decides whether the cost stays with the contractor or slides back toward you.

Practical rule: If a vendor can't prove coverage clearly and cleanly, they are not ready to work on your property.

Property managers who take this seriously usually avoid the worst disputes before they start. They verify coverage, require proper contract language, and reject vague assurances like “we've always had insurance” or “our agent is sending something over.”

What a good minimum package looks like

Before a grounds care professional starts work, confirm that the company has coverage built for commercial operations, not just a certificate generated to satisfy procurement. A polished PDF doesn't mean the right policy is in place.

Use this simple standard:

- Match the legal entity: The insured name on the certificate must match the entity signing your contract.

- Match the job timeline: Policy dates must cover the entire service period.

- Match the work scope: If the contractor handles irrigation, chemical application, tree work, or design input, the coverage structure should reflect that reality.

- Match the contract requirements: Limits and endorsements must align with your vendor agreement, not the vendor's preferences.

If you're reviewing landscaping partners more broadly, this property manager checklist for choosing a commercial landscaping partner is a useful companion to your insurance review process.

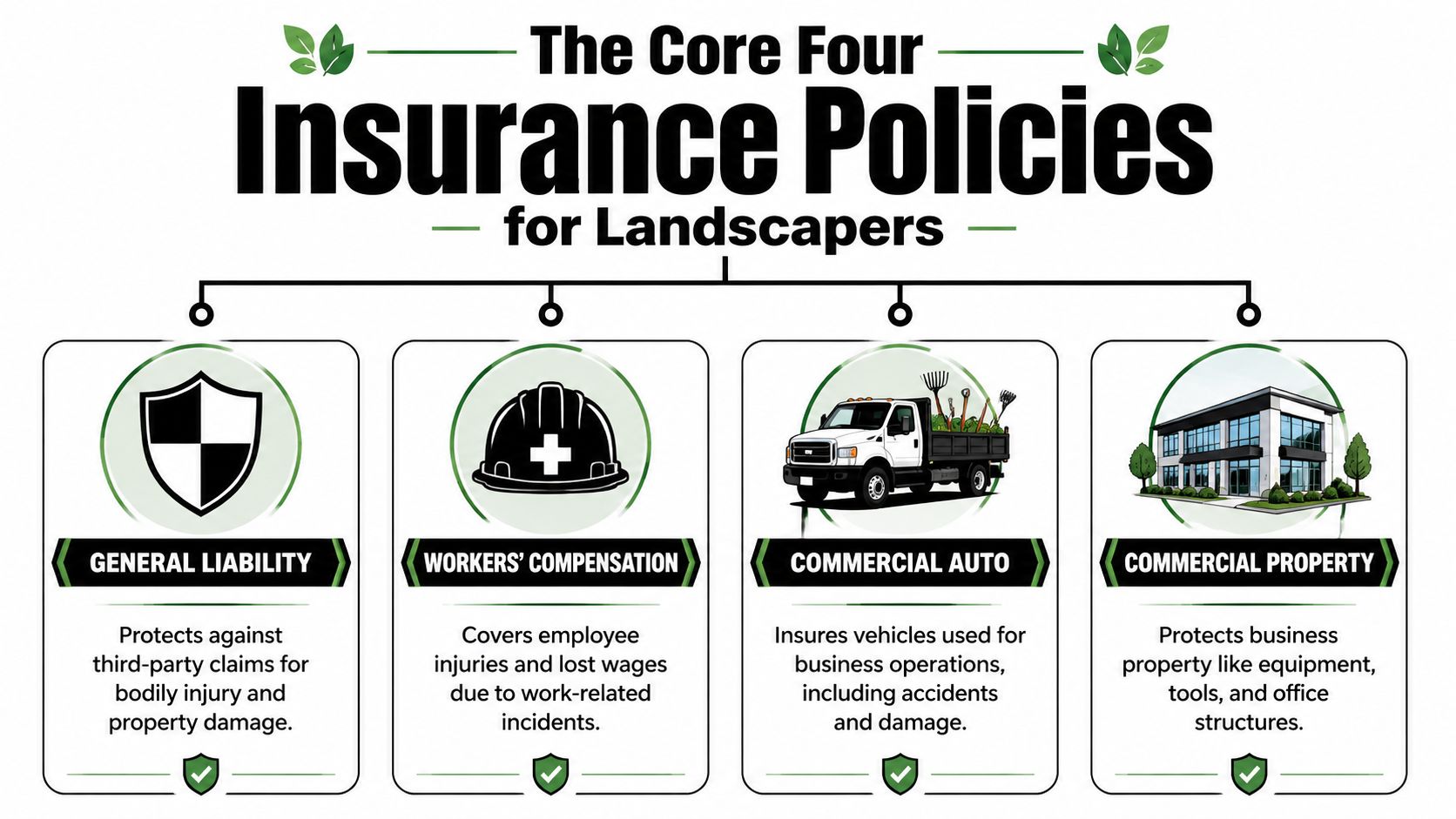

The Core Four Insurance Policies for Landscapers

Property managers get into trouble when they treat every insurance line as interchangeable. They aren't. Each policy solves a different problem, and if one is missing, your contract has a hole.

Insureon reports average monthly costs of $51 for general liability, $169 for workers' compensation, $204 for commercial auto, and $88 for commercial umbrella, with standard general liability limits of $1 million per occurrence and $2 million aggregate. Those figures matter because they show these coverages are standard operating tools, not exotic add-ons.

General liability

This is the slip, trip, and oops policy. It's the first line of defense when the professional causes third-party bodily injury or property damage.

Examples include a mower throwing debris into glass, a crew damaging site fixtures, or a visitor getting hurt because equipment was left in a pedestrian area. If you only verify one policy, this is the bare minimum. But bare minimum thinking is how claims leak back to the property.

Workers' compensation

This is the barrier between an injured worker and a messy fight over who should pay. Landscaping is physical work. Crews lift, cut, trim, dig, drive, and work around heat and uneven ground. Someone will eventually get hurt.

When workers' comp is in place, the contractor's employee typically has a defined path for medical and wage-related benefits through that system. Without it, your property can get dragged into the fallout, especially if site conditions are disputed.

Commercial auto

This is the policy many managers forget to inspect closely. That's a mistake. Landscaping companies live out of trucks, trailers, and route schedules. A vehicle accident entering your property, moving through a service lane, or backing near a building can trigger expensive damage and injury claims fast.

Don't accept assumptions that personal auto coverage is “good enough.” It isn't a commercial risk solution. If you want a plain-language outside reference on contractor liability structures, this guide to protecting your contracting business gives a decent overview.

Commercial umbrella

Umbrella coverage is the safety net above the safety net. It sits over certain primary liability policies and can respond when a large claim exhausts underlying limits.

You may go years without needing it. Then one severe incident happens, and it becomes the most important line on the certificate.

A vendor with only base policies may be technically insured and still not be financially prepared for a serious loss on a high-value property.

Here's the practical breakdown:

| Policy | What it protects against | Why you should care |

|---|---|---|

| General liability | Third-party injury and property damage | Protects your site from routine operational accidents |

| Workers' compensation | Employee injury claims | Reduces the chance that worker injuries become your legal problem |

| Commercial auto | Vehicle-related losses from business use | Covers a major source of overlooked exposure |

| Commercial umbrella | Large losses above primary limits | Adds protection when one claim gets expensive fast |

Advanced Coverage for Specialized Landscaping Risks

The amateur view of landscaping risk is simple: someone gets cut, someone breaks a window, insurance handles it. That view is outdated.

Modern commercial landscaping often includes irrigation audits, controller adjustments, repairs, water management recommendations, chemical use, and scope decisions that look a lot like professional judgment. That means some of the most damaging losses don't fit neatly inside a basic mowing contractor profile.

The risk most managers underrate

The biggest blind spot is water.

Minico notes that the highest-severity claim may not be a “landscaping accident” at all, but a water-loss event tied to control systems or delayed leak detection, and insurers specifically flag exclusions involving weather-related damage and pollution. That should change how you review every irrigation-heavy vendor.

If a controller malfunctions, a line leaks unnoticed, or a repair is done poorly, who pays for damage to turf, hardscape, tenant areas, neighboring property, or structures? Don't assume the answer is “general liability.” Sometimes it is. Sometimes it isn't. That's exactly the problem.

The most expensive landscaping claim on your property may start as a water-management issue, not a mowing mistake.

For managers overseeing irrigation-intensive sites, this commercial landscaping water management resource is worth reading because it frames irrigation as an operational system, not just a maintenance line item.

Coverage that separates basic vendors from professional operators

Ask sharper questions when the vendor's scope goes beyond basic maintenance:

- Pollution liability: If the contractor applies herbicides, pesticides, fertilizers, or handles fuel on site, ask how pollution-related claims are addressed.

- Professional liability or E&O-style coverage: If the company gives design advice, irrigation recommendations, controller programming, or audit-based guidance, ask whether errors in judgment are covered.

- Tools and equipment or inland marine coverage: If crews move high-value equipment between properties, ask how theft or transit damage is insured.

- Property damage exclusions: Don't ask “Are we covered?” Ask, “What water-related exclusions apply to this exact scope?”

A serious property manager doesn't stop at certificate collection. You need to pressure-test the mismatch between what the vendor says they do and what the policy contemplates.

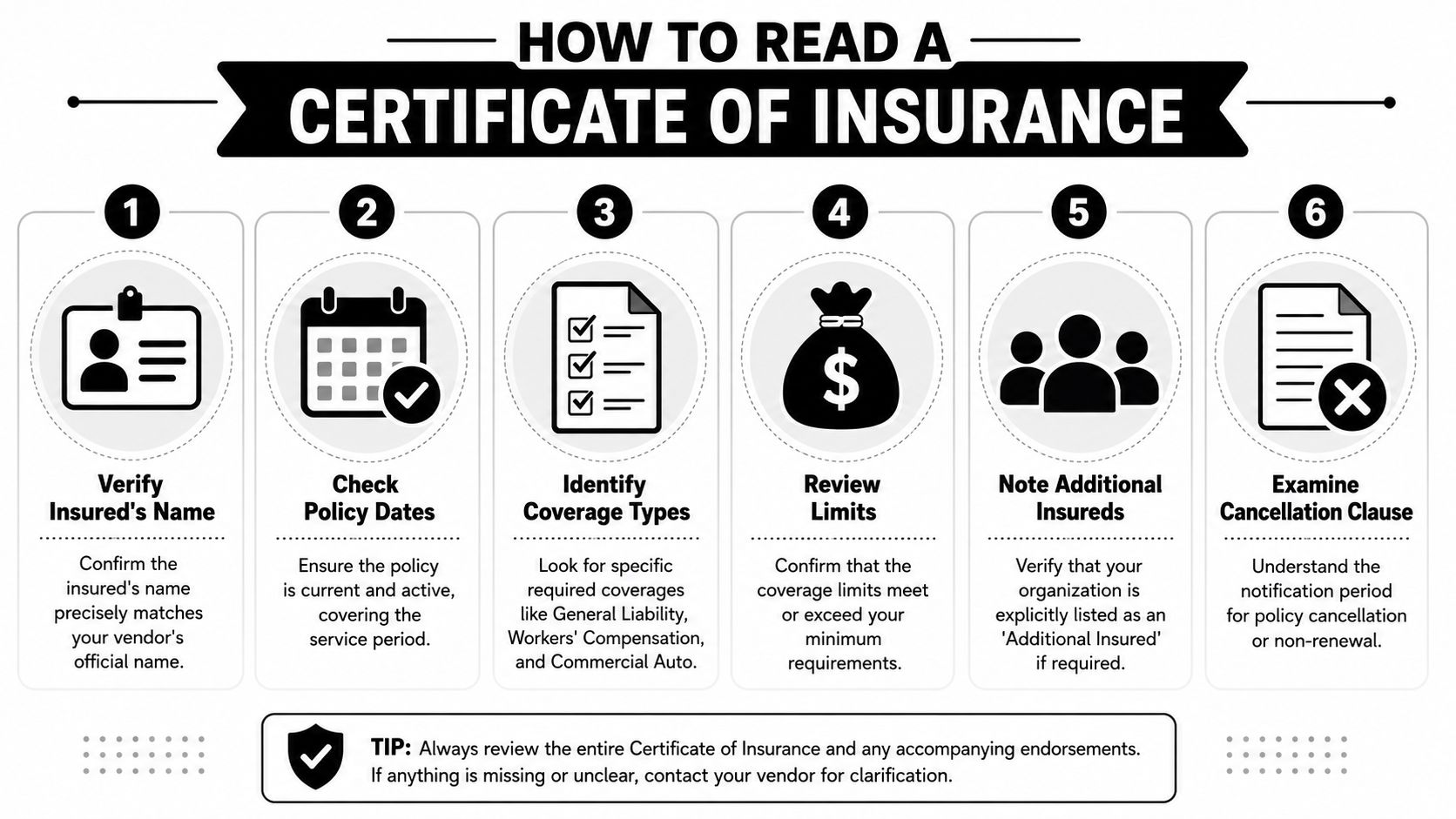

How to Read a Certificate of Insurance

A certificate of insurance, usually an ACORD 25, is a snapshot. It is not the policy. It does not rewrite exclusions. It does not create coverage by itself. But it can tell you very quickly whether the vendor deserves deeper trust or immediate pushback.

Start with identity and dates

Most certificate reviews fail because the reviewer jumps to the limits box first. Start higher.

- Verify the producer. You want a legitimate insurance agency or broker listed, not a homemade document that looks official.

- Check the named insured. The business name must exactly match the legal entity in your contract. If your agreement is with one LLC and the certificate names another company, stop.

- Review the policy dates. Effective and expiration dates must cover the full service term. If the policy renews mid-contract, your tracking system should catch that.

These details sound administrative. They aren't. A mismatch here can wreck your risk transfer before a claim ever starts.

Then verify the parts that actually protect you

Once identity and dates are clean, review the coverage lines and description box with a contract in hand.

Focus on these items:

- Coverage types: Look for the policies your contract requires, not just whatever the vendor chose to buy.

- Limits: Confirm the certificate reflects the minimums you demanded.

- Additional insured wording: If your contract requires it, the certificate should reference it, and the endorsement should be available on request.

- Operations description: This box should identify your organization or project when appropriate.

- Cancellation language: Read it, but don't overestimate it. Certificate notice language is often weaker than managers assume.

A fast review table helps:

| COI item | What to check | Red flag |

|---|---|---|

| Insured name | Exact legal entity match | Trade name only, wrong LLC, or affiliate mismatch |

| Policy dates | Active through service period | Policy expires during contract term |

| Coverage lines | Required policies listed | Missing auto, workers' comp, or umbrella |

| Limits | Meets your contract | Lower limits than your agreement requires |

| Description box | References required status or operations | No mention of additional insured or project details |

If the certificate says “for information only,” believe it. You still need endorsements and contract language to lock in real protection.

If you manage insurance reviews across multiple vendor types, not just outdoor service professionals, this insurance verification process guide for homeowner-related checks can help you tighten your internal review habits.

Use this repeatable checklist every time:

- Name match first: Legal names must align before you review anything else.

- Dates before dispatch: No active policy, no work order.

- Scope match: Irrigation, chemicals, tree work, and subcontracting should trigger deeper review.

- Endorsements on request: Don't settle for verbal confirmation.

- Calendar renewals: Expiring certificates create silent gaps.

Essential Contract Clauses for Risk Transfer

Insurance without contract language is incomplete. The certificate tells you what the vendor appears to carry. The contract tells you how that insurance should respond in relation to your property.

If you want real risk transfer, three clauses are essential.

Additional insured status

This is the clause that can give your organization rights under the vendor's liability policy for claims tied to their work. Without it, you may be standing beside the contractor in a dispute instead of stepping into their coverage structure.

Use direct language and have counsel adapt it to your form:

Contractor shall name Owner, Property Manager, and their respective affiliates, officers, directors, members, managers, and employees as additional insureds on applicable liability policies for claims arising out of Contractor's ongoing and completed operations.

Claim handling gets cleaner when your status is already built into the insurance framework.

Primary and noncontributory wording

You don't want your own insurance carrier paying first when the contractor caused the loss. That's what this clause addresses.

Contractor's insurance shall be primary and noncontributory with respect to any insurance maintained by Owner or Property Manager, except to the extent prohibited by law.

That sentence does real work. It tells the parties, and ideally the insurer through endorsement, that the contractor's policy sits in front of yours for covered claims.

Waiver of subrogation

Subrogation is an insurer's effort to recover money after paying a claim. A waiver helps reduce the chance that the contractor's insurer pays the loss and then turns around and sues your ownership group or management entity.

Contractor waives, and shall cause its insurers to waive, all rights of subrogation against Owner and Property Manager, and their respective affiliates, officers, directors, members, managers, and employees, to the extent of insurance proceeds received.

Here's the blunt advice. If your landscaping contract doesn't require all three, your risk transfer program is soft.

Use this contract review lens:

- Additional insured gives you access.

- Primary and noncontributory sets payment order.

- Waiver of subrogation helps prevent recovery actions against you.

If you're revising service agreements more broadly, this commercial landscape contract overview is a useful reference point for tightening vendor documents before renewal season.

Real-World Scenarios and Best Practices

Claims get easier to manage when you can identify the likely policy response before the incident report is even finished. That's not theory. It's operating discipline.

NerdWallet notes that strong landscaping risk management centers on the most common claims: third-party bodily injury and property damage, employee injuries, and mobile equipment theft, with median U.S. premiums of about $1,400 per year for general liability and $4,000 per year for workers' comp. That lines up with what property managers see repeatedly.

Three claims that happen fast

A crew member slips while unloading equipment and suffers a serious injury. The first policy in play is workers' compensation. Your protection improves if the contractor has the coverage required by contract and your site team documented who was on site and when.

A mower throws a rock through a storefront window before opening hours. That's usually a general liability event because it involves third-party property damage caused by the contractor's operations. If you required additional insured status properly, your company is in a stronger position during claim handling.

Irrigation overspray hits a walkway every morning, algae builds up, and a visitor falls. In such cases, claims become messy. The argument may involve maintenance practices, notice, premises conditions, and whether the contractor's operations caused the hazard. Good contracts and good records matter as much as the policy name.

The operating habits that keep you out of trouble

The best property managers don't improvise vendor insurance control. They systematize it.

- Track expirations centrally: Use your property operations platform or vendor file system to flag renewals before coverage lapses. If you're comparing operational tools, this guide for property managers on software can help you think through workflow support.

- Require incident reporting fast: Your contract should require prompt notice after injuries, property damage, vehicle accidents, or suspected irrigation failures.

- Audit scope creep: If a vendor starts doing irrigation diagnostics, chemical work, or subcontracted repairs beyond the original agreement, revisit insurance requirements.

- Keep endorsements on file: Certificates are useful. Endorsements are stronger evidence.

Good vendor management is repetitive by design. The same checks, every renewal, every site, every contractor.

Frequently Asked Questions about Landscaping Insurance

What does per occurrence mean compared with aggregate?

Per occurrence is the maximum a liability policy can pay for one covered incident. Aggregate is the maximum it can pay across covered claims during the policy period. If a certificate shows both, don't confuse the bigger total with the amount available for a single event.

Why do I care whether a landscaper carries workers' compensation?

Because injured workers create legal and financial exposure fast. If the contractor lacks proper workers' comp, their injury problem can become a property problem, especially when site safety allegations follow.

Is personal auto insurance enough for a landscaping vendor?

No. A landscaping company uses trucks, trailers, and vehicles for business operations. You should require commercial auto coverage, not assumptions.

How often should I request updated certificates of insurance?

At minimum, request updated certificates at renewal and before any new contract term or scope change. If the work is continuous, track expiration dates so you're not discovering a lapse after an incident.

Is a certificate of insurance enough by itself?

No. It helps you screen vendors, but it doesn't replace endorsements or contract language. If your requirements include additional insured status, primary and noncontributory wording, or waiver of subrogation, get proof those requirements were issued.

If you're evaluating commercial grounds care vendors and want a partner that understands irrigation risk, water management, responsive service, and the operational demands of commercial properties, Prestonwood Commercial Landscape Services is worth a close look. They serve Dallas-Fort Worth and San Antonio with a long-term, property-manager-focused approach built around maintenance, irrigation, construction, and consistent site standards.

{kind=link}

{kind=link}

{kind=link}

{kind=link}